Accounting Rules: A Clear and Practical Guide for Everyday Use

|

17 January 2026

|

17 January 2026

Accounting rules are the foundation of how financial information is recorded and understood. They help businesses and individuals track money accurately, avoid confusion, and maintain financial discipline. Knowing these rules is essential for anyone involved in handling finances, whether for personal use, studies, or business operations.

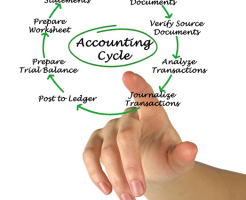

Meaning of Accounting Rules

Accounting rules are standard principles that guide the recording of financial transactions. These principles ensure that income, expenses, assets, and liabilities are recorded in a consistent and logical manner. When accounting rules are followed correctly, financial records remain transparent and trustworthy.

Core Rules That Govern Accounting

Every accounting entry is based on basic rules that determine how money movements are recorded. These rules help identify which account increases and which decreases during a transaction. Proper application of these rules ensures accuracy in financial statements.

Role of the Double Entry Principle

The double entry principle states that every financial transaction has two sides. When one account is increased, another account is affected in the opposite way. This balance helps maintain equality in the accounts and makes error detection easier. It also supports the fundamental accounting structure used worldwide.

Simple Steps to Record Transactions

To record any financial transaction correctly, a structured process is followed:

- Understand the nature of the transaction

- Identify the accounts involved

- Decide how each account is affected

- Record the transaction systematically

- Verify the entry for accuracy

Following this method helps maintain organised and reliable financial records.

Different Methods of Accounting

Accounting rules allow two common methods for recording transactions. One method records transactions only when money is exchanged, while the other records transactions when they occur, regardless of payment timing. Choosing the right method depends on the nature and size of the business.

Common Errors That Affect Accounting Accuracy

Mistakes in accounting usually happen due to carelessness or lack of understanding. Some frequent issues include recording incorrect amounts, missing entries, ignoring asset value reduction, and mixing personal and business finances. Regular review helps prevent such problems.

Best Practices for Applying Accounting Rules

- Keep financial records updated

- Review transactions regularly

- Maintain proper documentation

- Follow consistency in accounting methods

These practices improve financial control and long-term accuracy.

Conclusion

Accounting rules provide structure and clarity in financial management. When applied correctly, they help individuals and organisations maintain control over finances and make confident decisions.

With Zlendo Suite, users can access smart tools and insights that simplify financial understanding and help apply accounting principles more effectively in real-life situations.

Disclaimer

Accounting rules and practices may differ based on location, industry, and regulatory requirements. Readers are advised to consult qualified accounting professionals before making financial or business decisions.